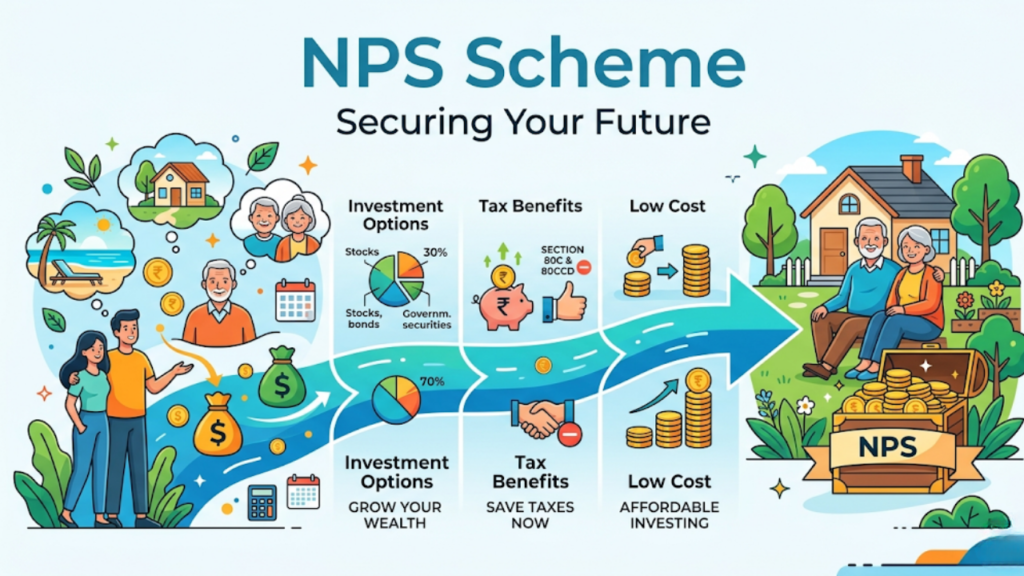

If retirement is one of the most crucial financial decisions of our lives, then the NPS scheme (National Pension System) makes this journey easy, flexible, and transformational. NPS (National Pension System) is a government-backed retirement savings scheme regulated by the Pension Fund Regulatory and Development Authority of India, providing long-term investment through periodic monthly contributions, which form a corpus for individuals at retirement age.

In the fast-evolving financial landscape, relying solely on savings will not suffice. Best NPS scheme comes to your aid here with its market-linked returns, tax benefits, and flexibility in investment mix selection. Whether you are a salaried employee, self-employed professional, or fresh out of college, NPS offers you an organized option to ensure your future.

Exploring the NPS Gov10 walk-through guide, learning how to calculate your corpus using an NPS scheme calculator, gathering useful information about the benefits, and reviewing charts like ECG allocation.

What is the NPS Scheme

The NPS (National Pension System) was introduced to provide financial security in old-age, regulated by the Pension Fund Regulatory and Development Authority and backed by the Indian government. It is useful for creating a retirement corpus through regular investing in working life.

Due to its low cost, tax benefits, and flexibility, it is among the best NPS schemes for long-term financial planning.

Best NPS Scheme – Why It Matters?

Higher Retirement Savings

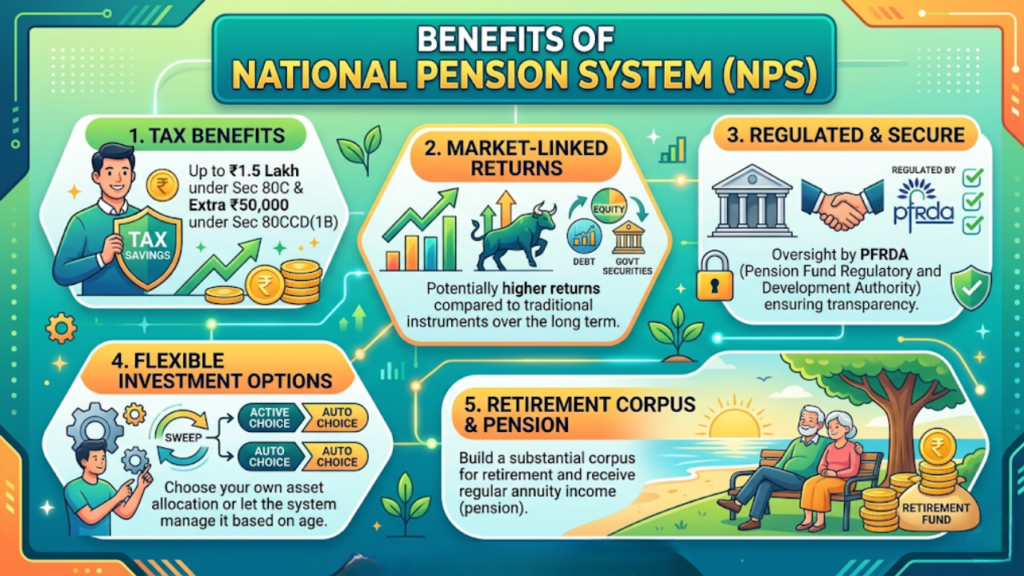

If you keep investing in the NPS regularly over a longer duration, your investment will grow owing to compounding. NPS is a market-linked scheme (investing in equity and debt) and is thus capable of giving better returns than conventional savings schemes. This aids in creating a wider retirement corpus.

Improved asset allocation (equity + debt)

- NPS enables you to split your investment into:

- E) Equity – Higher Growth

- Corporate Bonds (C) – for steady returns

- Government Bonds (G) – For Safety

This combination balances risk and return, keeping your investment safe while providing significant growth potential.

people invests in a Retirement fund to Save Tax.

Perhaps the biggest draw of NPS is its tax incentives:

- Deduction of up to ₹1.5 lakh under Section 80C

- Additional ₹50,000 under Section 80CCD(1B)

- Employers’ contributions also provide additional tax benefits

This means you are not only saving for retirement but also helping lower your taxable income.

Financial Security After Retirement

At the time of retirement:

- You can get up to 60 percent of your savings tax-free.

- The remaining 40% is used for generating a regular pension (annuity)

- It will make sure you have a steady income in the long run, even after stopping working.

Suitable for Everyone

The NPS scheme is flexibe and it can be opened in the following manner:

- Salaried employees (private & government)

- Self-employed individuals

- Business owners

Its low investment needs and flexibility allow anyone to invest as well as ensure their future.

Read also: Ladli Laxmi Yojna | AePDS Bihar | Rajiv Yuva Vikasam Scheme

NPS Scheme Details (Overview)

| Feature | Details |

| Scheme Type | Pension/Retirement |

| Regulator | PFRDA |

| Entry Age | 18–70 years |

| Lock-in | Till retirement (60 years) |

| Investment Options | Equity, Corporate Bonds, Govt Bonds |

| Returns | Market-linked (8–12% avg historically) |

| Tax Benefits | Up to ₹2 lakh deduction |

NPS Scheme Year – Investment Duration

NPS Scheme Year: The NPS scheme year is a period of time that requires you to stay invested till your retirement.

- Minimum: Until age 60

- Other Extensions: Can be extended up to 75 years

- Enable Partial withdrawal after 3 years

The longer the duration of your investment, = The more compounding benefits.

How Does An NPS Scheme Calculator Work?

NPS Scheme Calculator helps you estimate your retirement corpus based on:

- Monthly contribution

- Expected return rate

- Investment duration

Example Calculation:

Investing ₹5,000/month for 25 years at 10% return:

- Total Investment: ₹15,00,000

- Estimated Corpus: ₹65 70 lakh

This highlights the power of compounding in NPS.

NPS Scheme Chart (Returns Example)

This is a simplified chart of an NPS scheme:

| Years | Monthly Investment | Estimated Corpus |

| 10 | ₹5,000 | ₹10–12 lakh |

| 20 | ₹5,000 | ₹35–40 lakh |

| 30 | ₹5,000 | ₹90 lakh+ |

NPS Scheme Benefits

NPS: NPS is a Long-Term Investment Powerhouse with Added Benefits

Tax Benefits

NPS saves a multiple of taxes each year for you as follows:

- You can avail of a deduction of up to ₹ 1.5 lakh u/s 80C

- Another deduction of ₹50,000 under Section 80CCD(1B)

- Tax-deductible contributions from your employer are also contributed here.

That way, you are not only growing the retirement savings, but keeping the taxable income lower as well.

Low-Cost Investment

NPS, compared to other investment options such as mutual funds, stands out for having one of the lowest fund management charges.

- Lower fees – more of your money stays invested and grows.

- Flexible Investment Options

With NPS, your money is not obliged to be invested in one way

Choose Equity or Debt Allocation

Two modes available:

- Active Choice: You Allocate

- Automatic. We will do an auto-allocation based on age

- This makes it suitable for both new and experienced investors.

Retirement Security

Several factors make NPS more attractive than EPF.

- Tax-exempt withdrawal of 60% of the corpus at maturity

- Out of this, 40% you spend to but annuity (monthly pension)

Thus, it guarantees a consistent stream of income after retirement, reducing its financial burden.

Partial Withdrawal Facility

NPS is not fully locked in, and you can avail a partial withdrawal for emergencies such as:

- Children’s education

- Marriage

- Medical emergencies

This Base case study is a realistic example of what the quantifiable financials could look like.

Read also: WWW.ipcainterface.com | SSPMIS Bihar

NPS Scheme ECG (Asset Allocation)

NPS invests your money into three types of assets:

- E (Equity) – Invests in shares, a high-return but high-risk asset class

- Corporate Bonds (C)–medium risk and medium return

- G(Govt Bonds): Moderate risk-free assets that assure returns

Thus, you can change this combination according to your age and risk appetite to create an optimum and balanced char portfolio.

Post Office Option under NPS Scheme

How to Open an NPS Account: An NPS account can be opened through

- Banks

- Online platforms

- India Post

The Post Office option is especially beneficial for rural and semi-urban customers who prefer offline services and have trust in government organisations.

NPS Scheme PDF

This is all the NPS PDF document consists of.

- Scheme’s rule and regulation

- Investment guidelines

- Withdrawal and exit rules

- Tax benefits

- List of fund managers

It’s convenient for a guy who only likes to have all the genuine news & information before putting in some investment.

NPS Investment Guide – Step-by-Step Process

Starting NPS is simple:

- Therefore, visit its official website or your bank – financialservices.gov.in

- Step 1- Registration Form Filling (PRAN creation)

- KYC documents are to be submitted now (Aadhaar, PAN, etc.)

- Choose your fund manager & your asset allocation

- Make your first contribution

From there, you can continue to invest online or offline in your regular business, hassle-free!

Who Should Invest in NPS?

NPS is a suitable choice for just about anyone:

- Tax Planning, experiment with different tax demonstrations for Salaried people

- Self-Employed – Not enrolled in an employer-based pension, and hence, NPS helps in building one

- Good for long-term investors – best for creating wealth over the long-term (20–30 years)

- On-time retirement Planners – give you a strong financial backup

NPS is for people who are looking forward to spending their life after retirement in a very secure and financially blissful manner.

Conclusion

The NPS scheme is one of the most authentic and effective retirement planning tools in the country. All these features make it the most ideal NPS scheme, along with the concept of tax advantages and no restrictions on withdrawals. If you are going to invest in a risk-taking or a safe securities company, being flexible gives you the upper hand for your future security.

With a potential for significant growth in investments over the long term, provided you start early and invest consistently, NPS can help you build a sizeable retirement corpus that meets your financial independence goal.

FAQs

Is NPS better than PPF?

NPS returns are higher (all market-linked) while PPF returns are fixed and have safety.

Everything You Should Know About Investing in NPS

Minimum ₹500 per contribution

Can you take a distribution before you retire?

Yes, it is allowed to make a partial withdrawal after 3 years.

Is NPS safe?

Yes, Regulated by PFRDA & it is Safe.

What happens at maturity?

60% can be withdrawn tax-free

40% is available to be used to buy an annuity (pension)

Leave a Comment